Ever wonder how you build and action a specific trading thesis from start to finish?

Then pay attention folks

Time to look at #Bonds vs #Stocks

We’ll use $TLT vs $SPY

It’s another Options Education long-form blog coming your way

↓

↓

➠ IT ALL STARTS WITH HAVING A VIEW

With the equity risk premium at multi-year lows.

Options may offer a relative value opportunity to access a repricing of this premium.

I am looking to exploit this potential mispricing and get cheap access to the equity risk premium.

How does that sound to you?

↓

↓

➠ THE BACKGROUND

Investors started this year optimistic about bonds after last year’s market troubles.

However, the recent weakness in risk assets has once again been led by bonds.

Causing them to underperform stocks.

In other words…

The S&P has come down, but bonds have come down much more.

This raises questions about how much longer this dynamic can last.

↓

↓

➠ BACKING THE IDEA WITH DATA

So let’s say that amid this action in $SPY vs. $TLT, you think there’s a decent chance of a “catch-down” in equities.

Are there any charts backing that up?

Yes!

Keep reading…

↓

↓

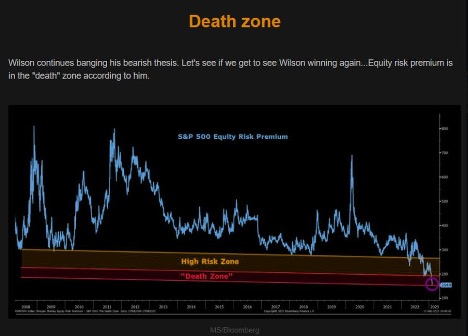

Let’s start by looking at the equity risk premium.

☞ Refer to the first #chart attached below ☜

(h/t @themarketear)

Risk premium refers to the excess return if investing in stocks over the risk-free rate of bonds.

So, you can see the equity risk premium collapsed because bond yields have gone up, and #SPX hasn’t sold off enough to match it.

↓

↓

Therefore, whilst we do think bonds might still have room to go lower…

Equities have even more room to go on the downside.

↓

↓

➠ THE VOL SKEW MATRIX

I am looking for a relative value opportunity to play this catch-down trade where stocks will start to underperform bonds.

Given that bonds have sold off so much and #yields, have come all the way back up to 4%.

↓

↓

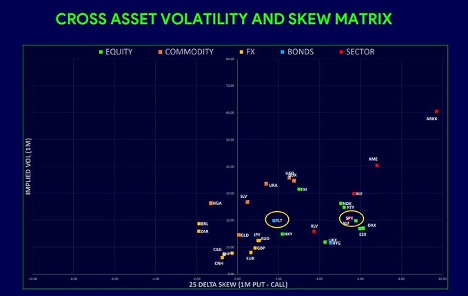

And using our Vol Skew Matrix, we can identify where the vol is.

Refer to the second chart below

The theme looks to be a general drift where volatility and skew have been rising.

Particularly for the equity landscape.

This presents a problem.

↓

↓

Equity skew has become much steeper in recent weeks.

So whilst ATM vols between the #SPY and #TLT may be equal, downside volatility is not.

Now, if we want to express the view of a heavier short position in equities, how can we neutralize this impact of a more expensive skew in equities versus bonds?

↓

↓

➠ THE TRADE

To do this, we recommend you use #PutSpreads instead of #Puts.

Thus allowing you to neutralize the impact of higher vols and skew in $SPX while creating a zero-cost trade…

And captures the scenario we are looking for where SPX sells off more than TLT from these levels!

↓

↓

Put spreads for both SPY & TLT have a 4 to 1 payoff if markets are down 5% by 31Mar.

Allowing us to capture the March #FOMC, as I think that might be the catalyst for #equities.

↓

↓

➠ Wondering the exact strikes I’m using so my TLT spread funds my SPY spread?

➠ How about the best strike selections now that some time has passed?

➠ And how do you size it for a 0-cost trade?

Well then, don’t forget that right now, you can get a free month of everything Options Insight has to offer!

Just follow the me on Twitter @options_insight and use code RV2023 when you checkout.

I provide these types of trade ideas several times a week on #equities #bonds #commodities #forex #crypto #sectors

… and that’s a wrap on The Anatomy of a Trade Idea.

Let me know what you think in the replies!

Also, if you enjoyed this info, please drop a reply as it helps the algos push more people it

Cheers! Markets