This post is a selection of insights from my reports to subscribers this week, showcasing how I build the contextual framework to find daily trade ideas. This is a repeatable process aimed at finding high-risk-reward trades. Note that the onus is on the subscriber to pick and choose which trades fit their overall risk.

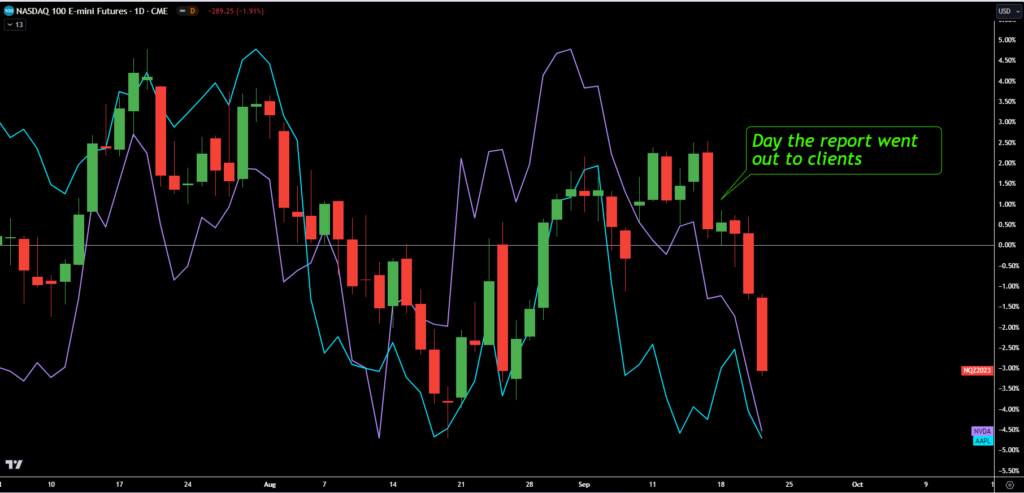

Big Tech Names Face Fragility

I started the week warning subscribers that big tech names, the likes of Apple or NVIDIA, could have more correcting to do, and that would impact broader indices due to their massive weightings. I reminded subs that the large-cap tech (AI-related) names had moved up to stretched multiples of around 30x, vs the rest of the market, which averaged about 17. Both assets are down for the week since our note.

Snapshot of $NDX, $AAPL, $NVDA on Sept 22nd:

Time to Hedge Uranium

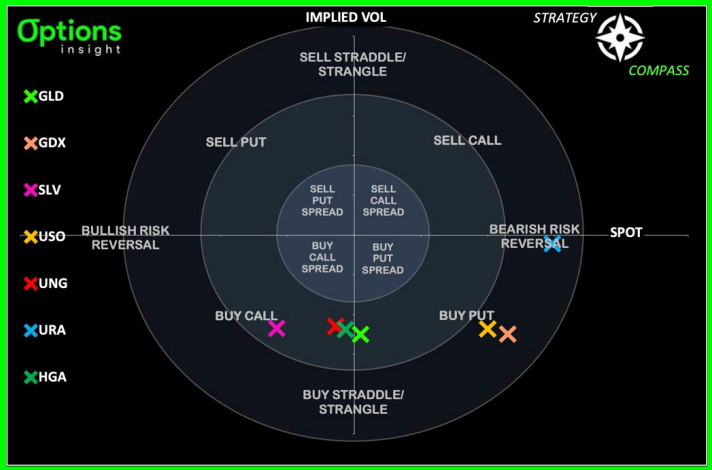

The same day (Sept 18th), I started to grow worried that the Uranium’s price action was looking somewhat parabolic. I suggested to those who own Cameco (part of my own long-term portfolio), that the timing was optimal to consider entering some hedges.

Snapshot of $URA implied vol (blue cross):

I, therefore, sent out a trade idea consisting of a combination of put spread buying vs naked call selling, also known as ‘put spread collar’ structures. This move made a lot of sense to me, provided one owns the underlying stock.

When implied vol in an asset is relatively high, as in the case of $CCJ, put spread collars are a great way to enter hedges and not bleed decay.

Snapshot of the trade idea on $CCJ:

Interested in learning the process/tools I follow, from thesis to trade idea? Join our next Free Options Trading Webinar

How Long Can This Low Vol Regime Last?

On Tuesday (Sept 19th), I highlighted the VIX seasonality, which typically sees a rise in the late Sep to October period which we are just entering into. Another interesting statistic is that the VIX has had its longest streak under 19 vol (80 days) since early 2020 just before COVID. While no one is expecting a super spike like that to occur, it goes to show how complacent vol markets had been getting.

The market conditions as of late had been ripe to pull more and more investors to short gamma even as the implied vol went to extremely low levels. Tentative evidence has appeared after the new launches of yield-earning ETFs such as Defiance 0DTE put selling fund.

This will attract a lot of retail money into the short-vol trade and is reminiscent of the XIV trade that triggered “Volmageddon” back in Feb 2018. This was a recipe that looked likely to build some fragility in markets.

Snapshot of the $VIX on Sept 22nd:

Interested in learning the process/tools I follow, from thesis to trade idea? Join our next Free Options Trading Webinar

Cheap Equity Protection

I found it an opportune time to double down the cautionary stance on equities given how cheap vol was, so that’s where part of the focus went into in the note I sent to subs on Sept 20th. I argued that while I agree vol was cheap, we also knew why.

As I explained: “The structural supply of index volatility has been growing through structured product issuance, systematic overwriting and now 0Dte options selling. On top of that, rates vol has been crushed as the market prices in the end of the tightening cycle.”

With this backdrop in mind, I put the following case out there for people to contemplate. What if the wild card is the FOMC dot plot coming out higher than expected, and bond yields break out of their range to a new high? Well, that’s actually what happened.

Snapshot of US 2y bond yield post-FOMC:

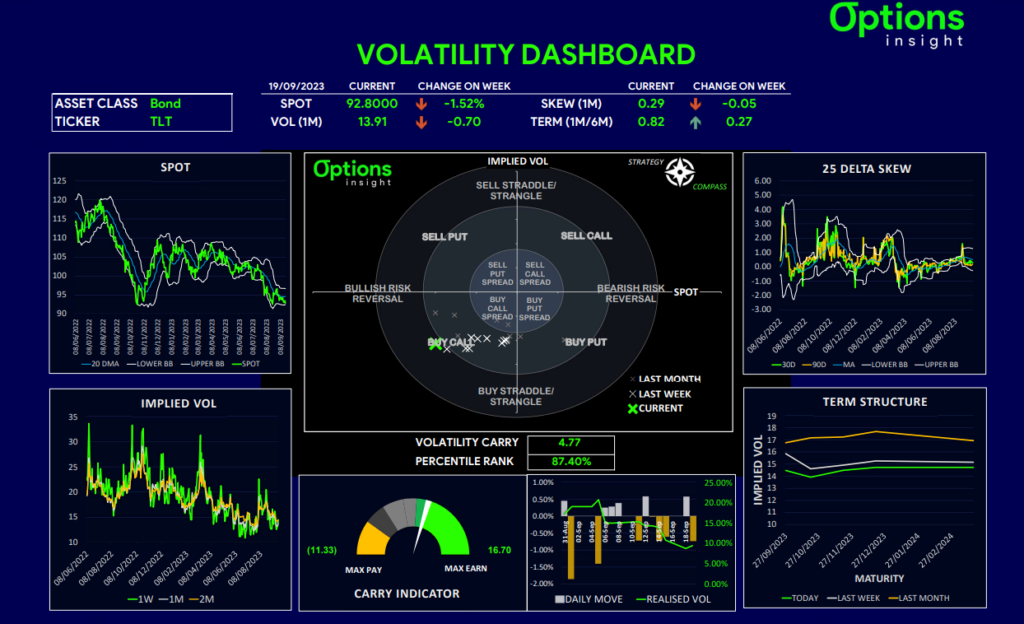

I felt finding ways to own cheap left-tail was a good opportunity in case the unexpected happened. The vehicle to express this idea was $TLT. I thought that another break higher in yields could fuel some more rate volatility as it has done every time the highs were broken.

Besides, the downside skew in TLT looked relatively cheap and vols had been crushed. 15Dec23 implied vol was down 3 points in the last month, which was a significant move.

Looking at the TLT vol dashboard showed BUY CALLS as the optimal trade. That obviously made sense if one were trying to play mean reversion. Since I was less convinced that bonds would have a sustainable bounce, I wanted to find ways to protect against a breakout in yields.

This was especially compelling to me on the basis that I didn’t think downside skew in TLT was being priced correctly to reflect the likelihood that rates vol spikes again if yields broke higher, as it happened.

I turned into the put ratio backspread to express this view, which will only kick into significant Greeks if we get a 5% or more move lower in TLT. The trade will then have decent short DELTA and long VEGA, which should work in our favour given how much vol has come down.

Snapshot of $TLT vol dashboard:

Snapshot of the trade idea on $TLT:

Interested in learning the process/tools I follow, from thesis to trade idea? Join our next Free Options Trading Webinar

Short-Term Pain, Mid-Term Gains?

While the Nasdaq correction may extend into early October, I still anticipate that a year-end rally may be in store.

In the near term, we have been calling for some postexpiry weakness and that seems to be playing out. We think that this leg of what looks like an incomplete correction could extend into early October and get as low as 340 on QQQ, but there are a few strong supports ahead.

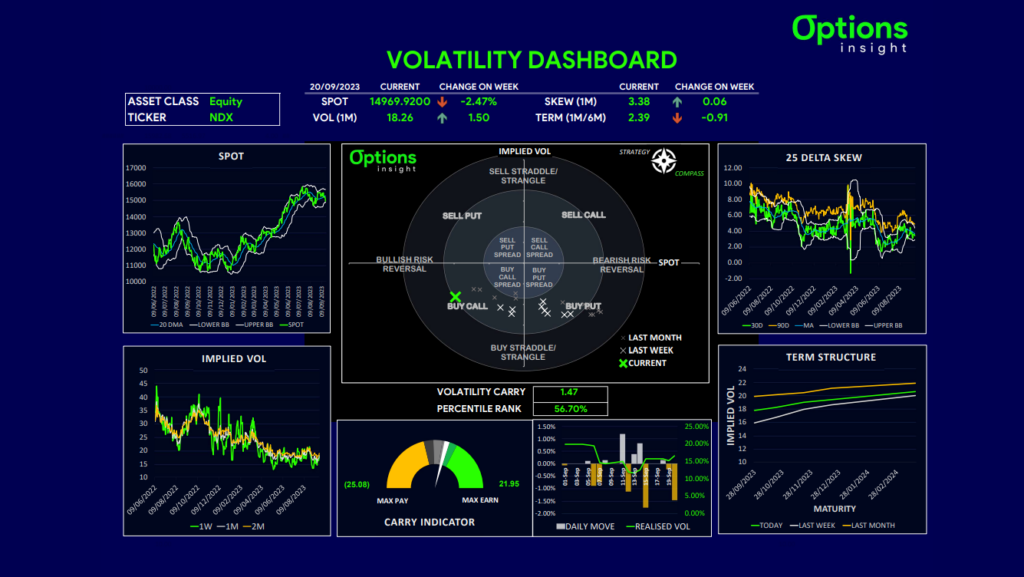

Snapshot of $QQQ price action:

I shared with subscribers the idea of entering long call ladder structures and funding them with put spreads as a nice way to dip your toes into a long position for a year-end rally. Using these type of structures keeps your cost down and theta bleed minimal.

Snapshot of $QQQ vol dashboard:

Snapshot of the trade idea on $QQQ:

Remember, not only do I share these trade ideas, but the ones I end up adding to my portfolio, are then tracked via a 20-30m weekly webcast that gives in-depth guidance. In it, you get to learn how to break down options trades by their Greeks and restructure trades in an optimal way to meet desired investment goals in real time. This weekly broadcast is part of our Macro Options Overlay.

Find below a taste of it via how I risk-managed carry trades.

And that’s a wrap for this week!

Remember, you now have a chance to build your knowledge base via our FREE Options Insight webinar!

You will learn the process and tools I follow, from thesis to trade idea and actual execution.

This is a unique chance to learn how to master simple options trading strategies straight from a 20+ year career.

Just click the link below!

Free Options Trading Webinar

σ

σ

Thank you for making it this far!

As always, if you have any questions, comments, and/or found this helpful, feel free to reach out and let us know at info@options-insight.com

Cheers!

Imran Lakha

Options Insight