Why tech vol isn't going back to old baselines

Every day into the close, there's a mechanical flow running through the tape. It comes from leveraged ETFs, and it's shaping tech vol in ways that don't show up on a chart.

Two-times and three-times leveraged funds are structurally required to buy high and sell low every single day. No option contract changes hands. It's part of why tech vol is trading at a structural premium the market probably won't unwind.

Here's the mechanic in plain English.

Say a 2x leveraged ETF starts the day with $100 of investor cash. To deliver double the return, the fund uses derivatives to control $200 worth of the underlying.

The stock rallies 10% on the day.

The fund's $200 position is now worth $220. Investor cash grows from $100 to $120. To maintain the 2x ratio for tomorrow, the fund needs to control $240. It's holding $220.

The gap is $20. The fund has to go into the closing bell and buy $20 more.

Same mechanic works in reverse. If the stock drops 10%, the fund has to sell $20 into weakness.

That's the plumbing. Mandatory buy-high, sell-low, every single day.

That's the exact behaviour of an options dealer who is short gamma. Same market impact, no options traded. Stealth gamma.

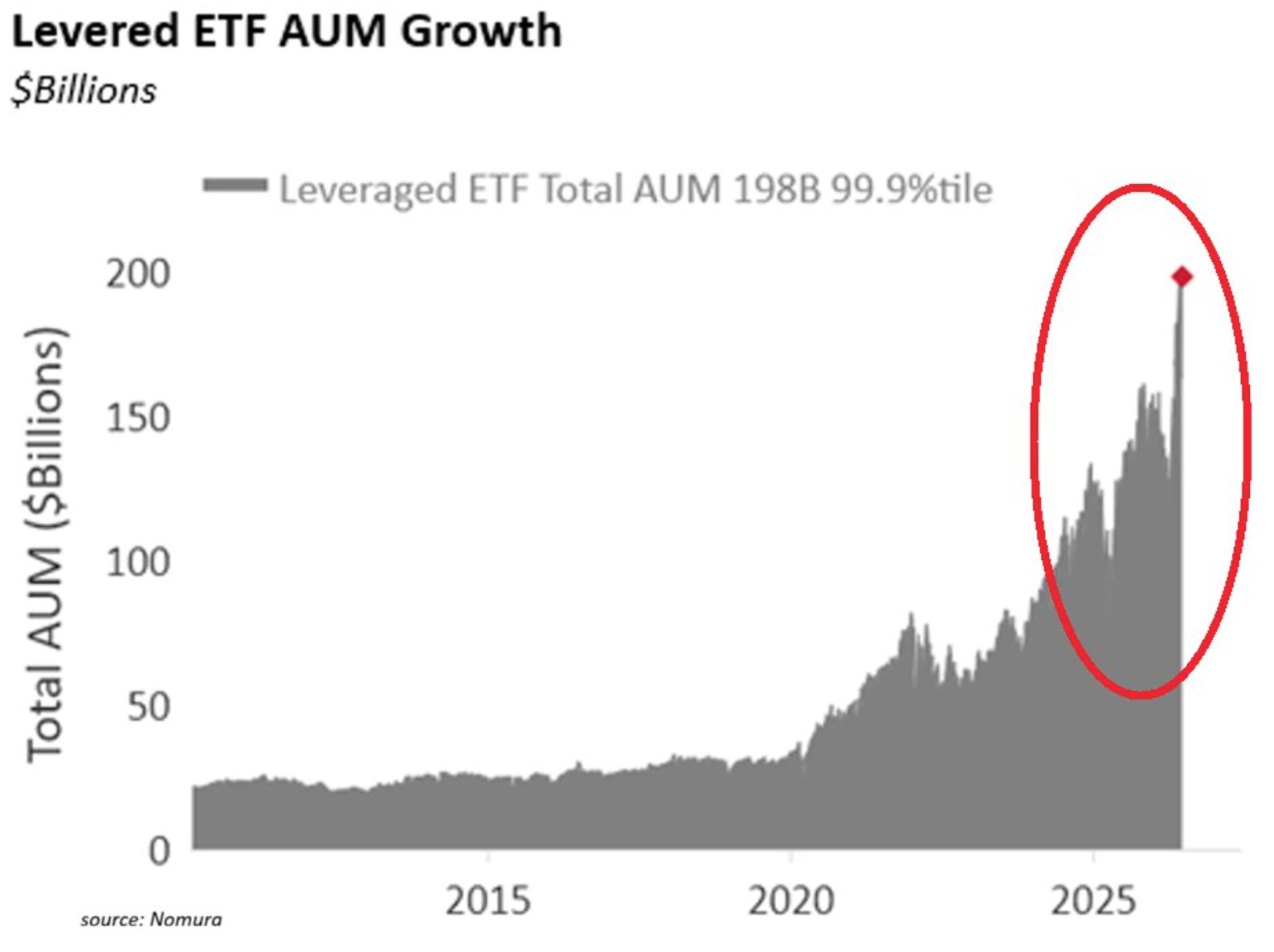

Total AUM in these products has exploded to $198 billion. The 99.9th percentile of the historical record. The plumbing has never been under this much pressure.

The single-stock version is where it gets dangerous.

Point this rebalancing math at an individual stock instead of an index and you're forcing large capital through a much narrower liquidity pipe. A sharp move in a single name triggers disproportionate forced buying or selling at the close. Intraday price action gets warped by the mechanical flow.

That brings us to tech vol.

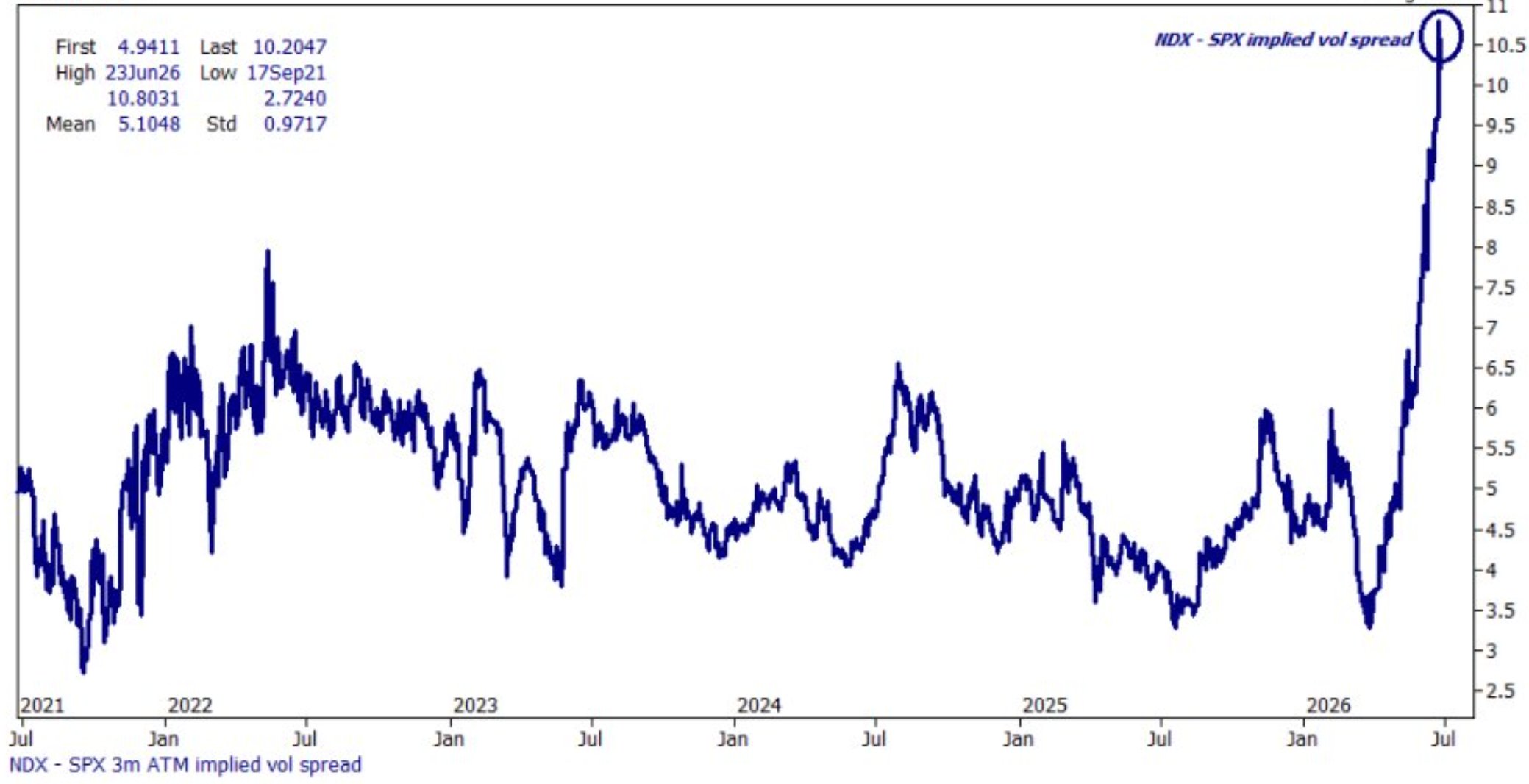

The NDX vs SPX three-month ATM implied vol spread just ruptured to a multi-year high of 10.2 vol points. The common read is that dealers are hoarding tech options to hedge the other side of these leveraged ETF swaps. That's part of it. The rest is the reflexive loop the plumbing creates.

Leveraged ETF forced-flow drives wider price gaps into the close. Wider gaps drive higher realised vol. Higher realised vol drives implied vol higher to reflect the real risk. Dealers bid options as an insulation layer against slippage on the predictable flow.

The loop feeds itself. Realised vol is genuinely elevated because the plumbing forces it there. Implied vol prices in that reality plus the insulation premium. The old NDX-SPX spread baseline was built in a world where these products didn't have $198 billion of AUM riding on them.

For me, the takeaway is that tech vol at a structural premium is a feature of the current market microstructure. Trading it as an overpricing that will mean-revert has become a losing bet. Trading it as a structural regime is closer to how the market is actually built now.

Reading market microstructure as it's actually built is what separates traders who last from traders who fade patterns that no longer exist. The framework I built across 20 years on bank options desks is below.

The bigger point extends beyond tech.

Any name where a large chunk of AUM sits inside a leveraged wrapper is now subject to the same plumbing. The vol regime you're looking at includes structural amplifiers that don't show up in standard option pricers. Reading the surface without reading the microstructure sitting behind it is trading half a story.

If you want to skip the masterclass and jump straight into our course, the Options Insight Advantage, this is the link.

Imran

Disclaimer (Your Gains & Losses, Your Responsibility): This content from Options Insight LLC (“Options Insight”) is for educational purposes only and does not provide individual investment advice or recommendations, nor should it be considered an offer to buy or sell any security. All information is general and not tailored to your specific objectives, financial situation, or risk tolerance. Employees of Options Insight may hold positions in the assets discussed. While we use sources believed to be reliable, we are not responsible for errors, omissions, or losses resulting from reliance on this content. Always consult a licensed investment professional.

Liked this? Imran writes one every market day. Get them direct to your inbox.